5 +1 charts on the results of the Hungarian crisis management compared to the Mediterranean region

EnglishDániel PalotaiAndrás Zsolt SzabicsBetween 2010 and 2017, the development of Hungary rose from less than 73 percent of the average development of the Mediterranean region to almost 90 percent. At the fifth station of the MNB's 5+1 series of articles on convergence, we present Hungary's macroeconomic convergence after 2010 compared to the Mediterranean countries of the euro area.

Although Hungary and the Mediterranean countries of the euro area faced similar macroeconomic difficulties at the outbreak of the 2008 crisis, the direction and manner of the crisis management sharply differed. Prior to the outbreak of the 2008 global crisis, Hungary and the ClubMed countries (Greece, Italy, Portugal and Spain) struggled with economic difficulties that were similar in many respects, although interspersed with individual differences.

The high budget and current account deficit, the substantial external indebtedness and the structural problems of the labour market resulted in deteriorating competitiveness and unsustainable growth path. These countries, deemed risky, were hit by the financial crisis particularly hard; the money market and financing problems led to major real economy downturn. While the Mediterranean countries applied the conventional, restrictive policy of crisis management, Hungary implemented structural reforms relying on unconventional and innovative instruments after 2010. The different instruments yielded completely different results.

The Hungarian novel and growth-friendly crisis management proved to be much more efficient than the traditional approach, built on austerity measures, applied by the Mediterranean countries. Contrary to the Mediterranean countries, in Hungary the budget and the real economy stabilised simultaneously, the excessive deficit procedure (EDP) was lifted in 2013, the independence of the economic policy strengthened (the IMF loans were repaid in full before maturity), and as a result of the permanent improvement in the macroeconomic fundamentals the economic outlooks of Hungary also improve continuously.

Hungary's convergence to the Mediterranean region, classified as advanced economies, is more than spectacular. Between 2010 and 2017, Hungary's GDP per capita approximated the average development of the ClubMed countries by 17 percentage points. More specifically, Hungary has already exceeded the development of Greece – due to the major economic downturn in Greece – by 9 percentage points in 2017, and at the same time it reached 96 percent of Portugal and stands at 78 and 76 percent of the development of Spain and Italy, respectively.

Due to the erroneous crisis management, the Mediterranean countries experienced lengthy economic recovery, and compared to Hungary they were able to reach their former performance much later.

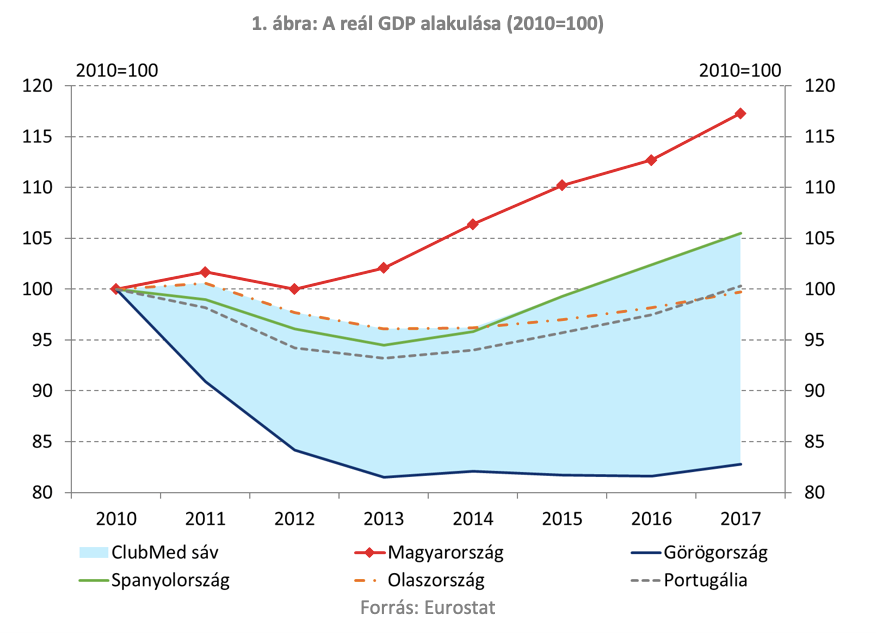

From 2010, the Hungarian crisis management was successful already in the short run, which was evidenced by the halt of the decline in economic performance, while all of the Mediterranean countries realised persistent downturn until 2013. As a result of the maturity of the post-2010 fiscal and economic reforms, the Hungarian economy has set on a dynamically expanding growth path from 2013. Hungary increased its real output by more than 17 percent between 2010 and 2017, while recovery in the ClubMed countries took substantially longer.

Although Spain exceeds its 2010 real GDP level already since 2016, Italy and Portugal hardly reached their own 2010 real performance in 2017. Greece appears to fall behind permanently, despite the more favourable external economic activity observed after the crisis, as it was not able to demonstrate any substantial economic growth since 2013. Hungary's post-crisis dynamic economic growth implies the success of the unconventional, innovative crisis management, supported both by the fiscal and monetary policy turn.

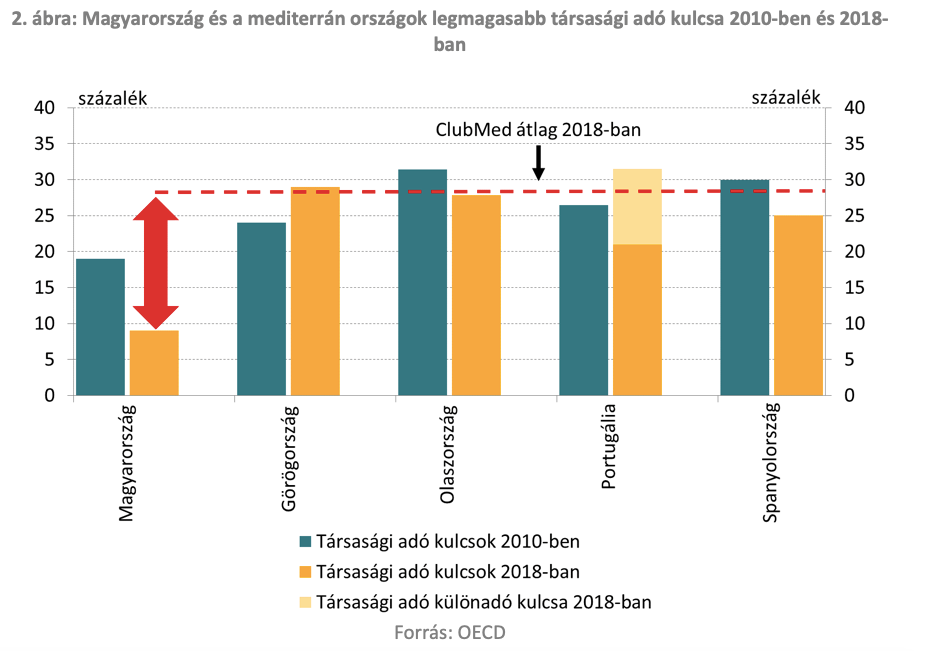

Since 2017, Hungary has the lowest (9 percent) corporate income tax rate in the European Union, while in the ClubMed countries the average corporate tax burden is high, being close to 30 percent.

In Hungary the small and medium-sized enterprises are key to the economy; almost two thirds of the people in employment work in the SME sector. Hungary was quick to realise that recovery from the crisis is conditional upon reducing the tax burdens of these enterprises, since this may increase the job creation capacity of this important employment sector. The first major step was implemented already in the second half of 2010, when the government expanded the range of enterprises eligible for the preferential (10 percent) corporate income tax rate.

As a result of the measure, the previous sales revenue ceiling of HUF 50 million was raised to HUF 500 million, which represented major tax cut for the SME sector. This was followed by fixing the corporate income tax flat rate at 9 percent from 2017, as a result of which Hungary has the lowest corporate income tax rate in Europe. The Mediterranean countries followed a different direction than Hungary: the corporate income tax rate rose in Greece and in Portugal, and the other countries were also unable to implement major tax cuts, and thus the corporate income tax is substantially higher than in Hungary.

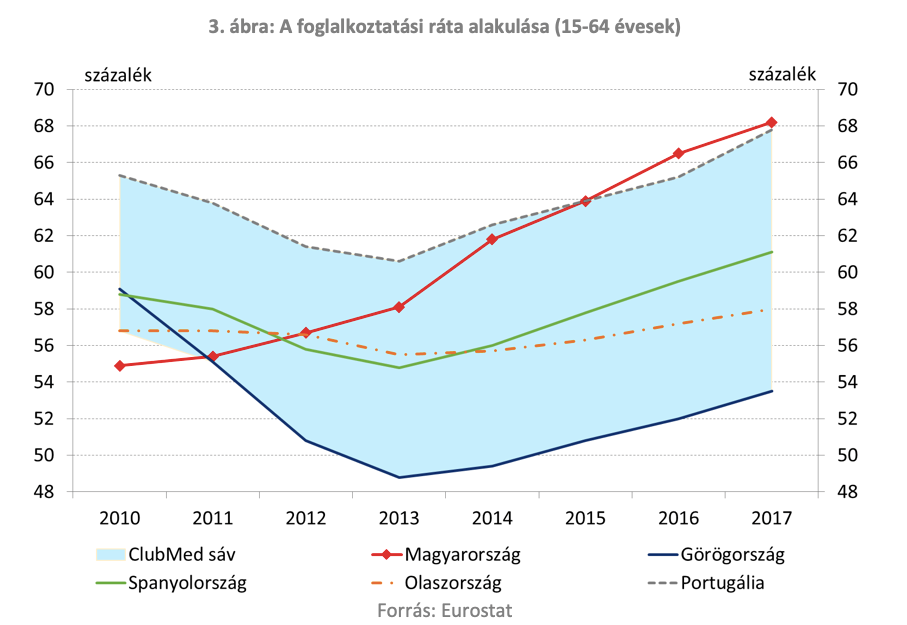

Within the European Union, the employment rate rose to the largest degree in Hungary since 2010.

The number of people in employment in Hungary exceeded 4.5 million for the first time in the recent months, thereby reaching a historic high. Prior to 2010, Hungary had the lowest employment rate in the European Union, which substantially curbed economic performance and also weakened the fiscal position. However, since its trough (55 percent) recorded in 2010, the Hungarian employment rate shows continuous increase, as a result of which it rose by 13.3 percentage points above 68 percent between 2010 and 2017. The growth in employment was supported by a variety of government measures in the past years.

The introduction and expansion of the Job Protection Action Plan, as well as the substantial decrease in the social contribution tax contributed to the retention of the labour force and to the fostering of labour demand to a large degree. The labour supply was supported, in addition to the introduction of the flat rate personal income and to the reduction thereof, by the establishment and continuous expansion of the family tax base allowances – tied to legitimate earned income –, by the rationalisation of the welfare transfers, the tightening of the early retirement schemes and the development of public employment. By contrast, the austerity measures implemented in the Mediterranean countries (e.g. raising the income tax, reducing wages and pensions, lay-offs in the public sector) did not support employment and real economy growth.

Accordingly, in the South European countries the post-crisis decline in the employment rate halted only in 2013, and then rose at a much lesser rate than in Hungary. Among the Mediterranean countries, the employment rate in Greece and Spain still substantially lags behind the pre-crisis level (61 and 66 percent, respectively), while Italy and Portugal reached the pre-crisis level, recorded in 2007, only in 2017.

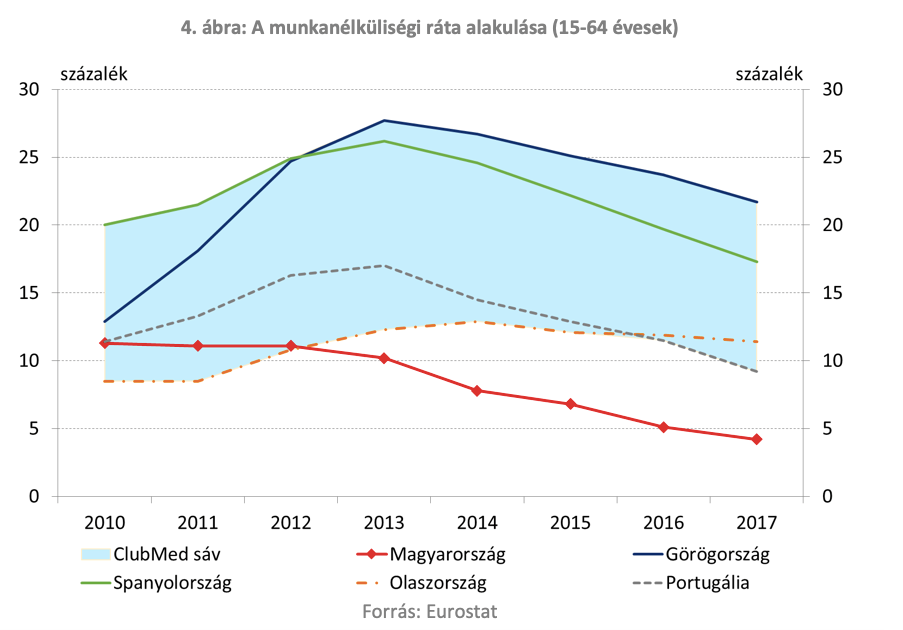

In parallel with the rise in employment, the Hungarian unemployment rate substantially declined in the past years – coming close to full employment, while unemployment in the Mediterranean countries is still high. As result of the economic policy measures aimed at the fostering of employment, the unemployment rate in Hungary is steadily declining since 2010. The Hungarian unemployment rate recorded the fifth largest decline (7.1 percent) in the European Union since 2010 (11.3 percent), as a result of which Hungary had the fourth lowest rate (4.2 percent) in 2017.

Moreover, in 2018 it declined to 3.6 percent, thereby coming close to full employment. By contrast, the unemployment rates in the Mediterranean countries substantially rose after the crisis and they started to decline only after 2013. The group of the South European countries still has not reached the pre-crisis levels and at present these countries have the highest unemployment rate in the Union (9-22 percent). The different trends in the unemployment rates also evidence the success of the Hungarian employment policy measures, as well as the negative effect of the adjustments on employment and economic growth.

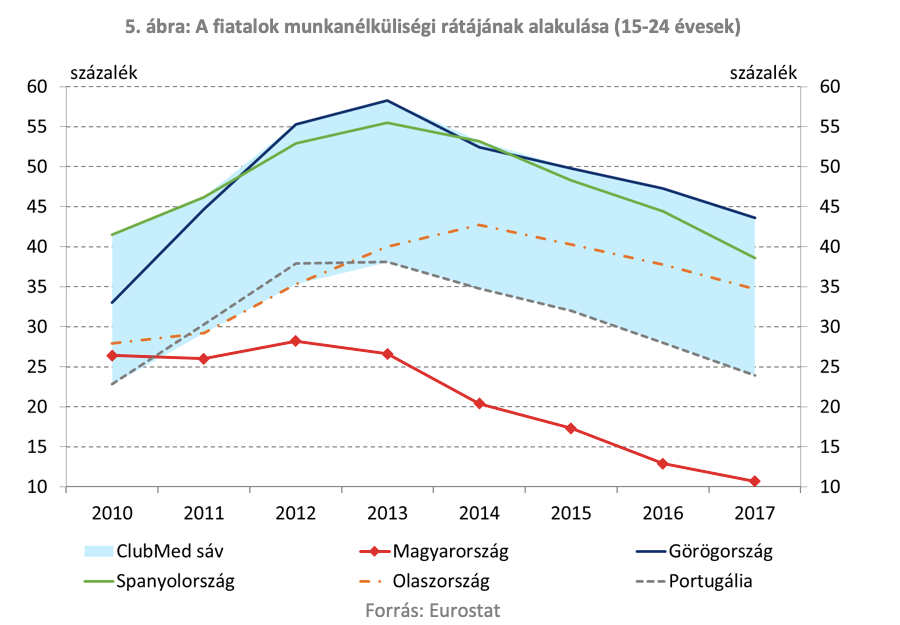

The labour market position of juvenile workers also improved substantially in Hungary after the crisis, while the indicators of the Mediterranean countries are significantly worse than the average of the European Union. In Hungary the unemployment rate of juvenile works, similarly to the total national economy indicator, materially declined, from 26.4 to 10.7 percent, between 2010 and 2017, and thus it is substantially lower than the EU average (16.8 percent) and also than the pre-crisis level (18 percent). Of the government measures taken after 2010 to foster employment, the allowances offered by the Job Protection Action Plan to juvenile workers (career starters, below 25 years) materially contributed to the improvement in the labour market position of juvenile workers.

Since 2012, the employment rate of this group rose by roughly one and half times. In the case of the ClubMed countries, the unemployment of juvenile workers rose more significantly after the crisis than in Hungary and in the EU, and the unemployment rates continue to exceed both the pre-crisis levels and the EU average. However, in the South European countries the unemployment rate of juvenile workers is traditionally higher, where the fact that young people live together with their parents longer may be partly the reason for and partly also the consequence of this. The unemployment of juvenile workers is more susceptible to the trends in economic activity, and thus the labour market position of this group deserves special attention from the governments.

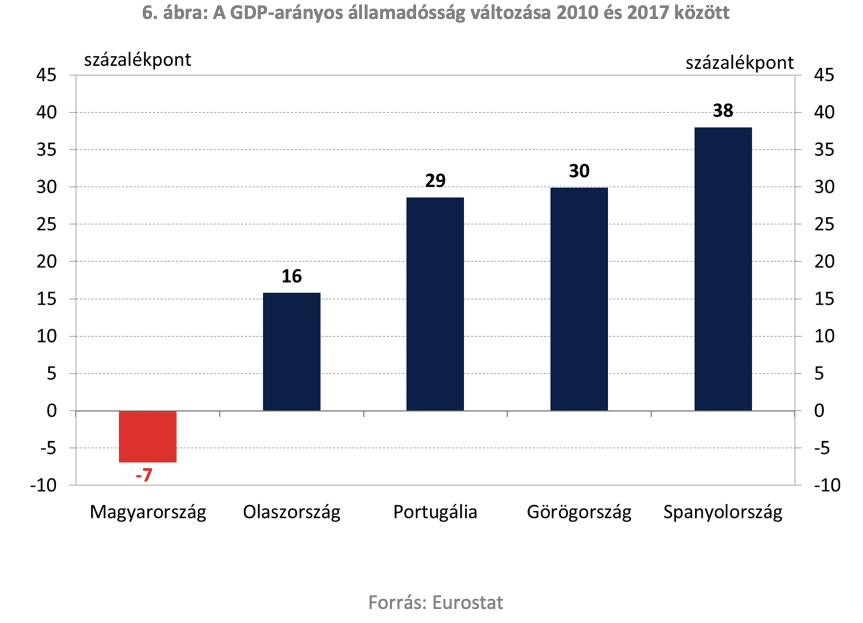

As a result of the disciplined fiscal policy and economic growth in excess of the EU average, Hungary's government debt has set on a declining path after 2011, while in the Mediterranean countries, the erroneous economic policy decisions stabilised the debt at high levels.

The government debt ratio is usually closely monitored by the market and economic agents, as well as by the international organisations and credit rating agencies. One of the reasons for this is that since it comprises the key macroeconomic indices, the changes in the government debt ratio is a relatively good indicator of the direction and quality of the economic policy and the macro economy. The other reason is that in the longer run high-level indebtedness hinders the country's economic convergence. Steady decline in the government debt to GDP ratio essentially depends on two conditions: government deficit stabilising at a low level and sustainable economic growth.

Hungary achieved major turn in both areas after 2010, while the Mediterranean countries were unable to cope with the challenges posed by the crisis. As a result of the fiscal reforms, in Hungary the general government deficit fell steadily below 3 percent from 2012 and the primary balance recorded a surplus for the first time after 12 years. The macroeconomic stabilisation also significantly improved the assessment of Hungary's risk, which was reflected in the major fall in the government interest expenditures. The latter was also substantially supported by the policy pursued by the central bank after 2013. As a result of the achieved macro-financial balance and the growth stimulating measures, the government debt to GDP ratio follows a persistently declining trend in Hungary. By contrast, due to the unsuccessful crisis management, the debt rose drastically and stabilised at a high level in the Mediterranean countries.