Kurzarbeit 2.0: the Hungarian wage subsidy scheme became more attractive

EnglishThe government considered the observations raised by the economic operators regarding the wage subsidy. As a result, the lawmakers modified the government decree including the provisions of the subsidization of reduced-time employment. We will show the main changes brought by the „kurzarbeit 2.0” and its quantitative effects.

Considering that the wage subsidy is one of the most significant measures of the government for curbing mass layoffs, it is crucial that the subsidy is of appropriate amount and the companies can obtain the support as smoothly as possible.

The broadening of the definition of „reduced worktime” might be regarded as one of the most important changes: the range of the work time reduction subject to the wage subsidy has been widened from the original 30-50% to 15-75%. Hence, the employee can become eligible for the wage subsidy even if the employer reduces his original worktime of weekly 40 hours to 34 work hours (meaning that the employee works only 1.2 hour less daily). According to the new rules, the employee will also become eligible for the subsidy even if the employer drastically reduces his worktime due to the decreased turnover (e.g. from weekly 40 hours to 8 hours).

Due to the fact that the reduction of worktime by 75% also became eligible, the theoretical maximum amount of the monthly state subsidy increased from HUF 75 thousand to HUF 112 thousand per employee.

Another important change is that those companies who are forced by the pandemic to reduce the worktime of their employees drastically (i.e. by more than 50%) will not be obliged to agree with their employees in individual development time – this change somewhat relieves the burden on the companies facing substantial decrease in sales. What is more, in such cases, the employer will not be obliged to “top up” the employees’ wage (increased by the wage subsidy) to their original base wage level (although this obligation still exists in case of work time reduction of 15-50%).

The overall headcount maintenance obligation stipulated in the original government decree would have caused difficulty to multiple companies. Under the “kurzarbeit 2.0” however, the employer will be obligated to maintain the employment of only those employees to whom the subsidy is applied for.

The administrative burden related to the utilization of the wage subsidy has also decreased – for example, there will be no need for amending the job contract for the subsidized period. As of the day on which the subsidy resolution is issued, the employment contract will be automatically amended as per the application for the duration of the subsidy in respect of the reduced-time employment and the individual development time. Another significant relief is that there will be no need for demonstrating the reason behind the reduction of work time.

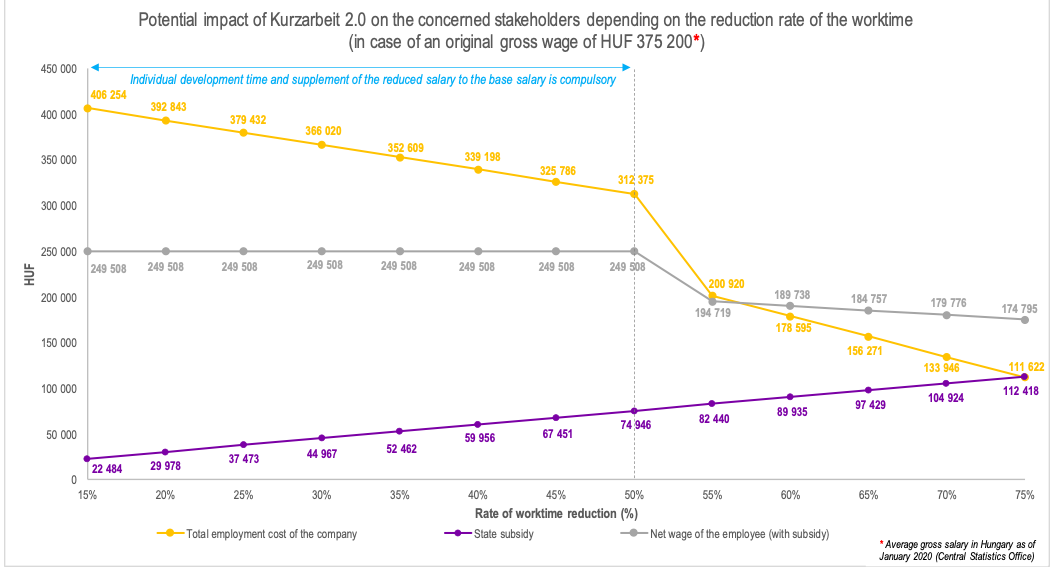

In the following diagram we will illustrate the expected impact of the “kurzarbeit 2.0” on the three concerned stakeholders depending on the rate of the work time reduction:

- on the employment cost of the employer (gross wage and payroll taxes)

- on the net wage of the employee and

- on the central government budget (amount of the state subsidy)

For the purposes of this illustration, we used the average gross salary of January 2020 (HUF 375,200) published by the Central Statistics Office on 31 March 2020. In addition, we assumed that

- the agreed compensation for the individual development time is in proportion with the original wage, and

- the employer and the employee do not agree on individual development time in case the work time reduction is larger than 50%.

The diagram reveals that the amount of the wage subsidy might reach even HUF 112 thousand in case of 75% reduction in work time (HUF 75 thousand was the maximum amount of the subsidy prior to the amendment of the relevant government decree).

If the work time of the employee is being reduced by 50% or 75%, the employment cost of the employer changes in proportion to the work time reduction (because in such case, agreement on individual development time is not compulsory).

For instance, the employment cost of the company decreases by 75% in case of a work time reduction of 75%. Nonetheless, the net wage of the employee – due to the state subsidy – will decrease in less extent than his work time. In case of a 75% reduction in work time, the net wage (incl. subsidy) of the employee will drop “only” by 30%.

It is worth noting that the net wage of the employee is unchanged up to 50% of work time reduction due to the individual development time and the “top-up obligation” of the employer according to which the wage of the employee (increased by the state subsidy) should reach his original base wage. However, the employment cost of the employer drops significantly in case of a work time reduction of 50% or more because in such case the individual development time is not compulsory and the employer’s “top-up obligation” ceases to exist.

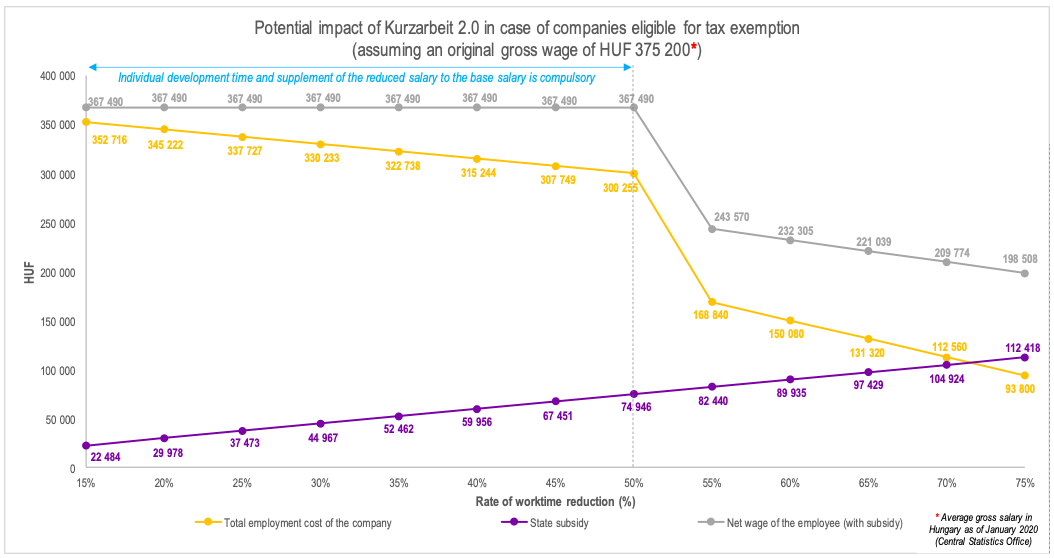

The impact of the “kurzarbeit 2.0” is more visible in industries that have been granted tax exemption by the government in its decree of March 18 (e.g. tourism, hospitality or entertainment sectors): in case of a work time reduction of 75%, the employment cost of these companies might even drop by 79% while the net wage of the employee decreases “only” by 20,4% due to the tax exemption and wage subsidy.

It is an interesting phenomenon that the net wage of the employee (incl. subsidy) is higher than the total employment cost of the company due to the combination of the tax exemption and wage subsidy.

In light of the above, it can be established that the Hungarian wage subsidy scheme became more flexible and it provides greater support to the companies for maintaining their workforce. Due to the special characteristics of the “kurzarbeit 2.0”, entities decreasing the work time of their employees by more than 50% can achieve a cost saving in a higher proportion.