MNB to stop government securities purchases and the Growth Bond Program

EnglishThe main enemy of the Hungarian National Bank (MNB) is inflation, so interest rate hikes will continue in 2022, Barnabás Virág said at a central bank press conference. MNB decided to phase out the government securities purchase program started in May 2020 and stop purchases immediately. The Monetary Council will also phase out the Growth Bond Program. MNB expects persistent price pressures. Core inflation, which excludes cyclical items, is expected to remain above the 4 percent tolerance limit throughout 2022.

Barnabás Virág, Deputy Governor of MNB emphasized that the key priority for the central bank is to reduce inflation and inflation expectations.

The domestic monetary policy has entered a new phase; and the Monetary Council will continue to tighten monetary conditions along two priorities.

On the one hand, the monthly cycle of base rate increases will continue. On the other hand, it is of paramount importance that all elements of the monetary policy toolkit help to achieve price stability as quickly as possible.

In the medium term, bringing inflation expectations down to the 3% central bank target will be crucial to achieving price stability.

Barnabás Virág said that MNB will continue to raise interest rates until the inflation outlook stabilizes near 3% and inflation risks become balanced.

At the same time, MNB completed the withdrawal of its crisis management tools.

Interest rate policy

The base rate was raised by 0.3 percentage points to 2.4 percent. According to the Deputy Governor of MNB, a long cycle of interest rate hikes is warranted in order to achieve the inflation target.

Base rate increases will continue in 2022. In addition, the one-week deposit facility rate should be increased at least to the same extent as the base rate," added Barnabás Virág.

The changes in the one-week deposit rate will also be permanently integrated into MNB's base rate hike cycle. By the end of the current phase, the base rate will once again converge with the one-week deposit rate.

Monetary transmission will be reinforced by raising the interest rate on overnight deposits by 0.8 percentage points to 2.4%.

This means that interest rate rises are also applied to the shortest part of the yield curve.

The 0.3 percentage point increase in the overnight and one-week collateralised lending rate to 4.1 percent maintains MNB's room for manoeuvre in determining the interest rate on the one-week deposit facility, so it could be further increased if necessary.

Government securities purchase program

MNB will phase out the government securities purchase program started in May 2020 and will stop purchases immediately.

At the same time, the central bank is ready to intervene with temporary and targeted government securities purchases, which would stabilize bond yields.

Growth Bond Program

The Monetary Council also decided to phase out the Growth Bond Program.

The central bank will not buy any new corporate bonds once the ongoing negotiations with issuers have been completed, added Barnabás Virág.

Inflation outlook

After peaking at 7.4% in November, the consumer price index is forecast by the central bank to decline gradually.

Inflation developments in the short term will be determined by the course of base and tax effects, the price cap on fuel prices and the extent of repricing at the beginning of the year.

The Monetary Council expects price pressures to persist. Core inflation, which excludes cyclical items, may remain above the 4% tolerance limit throughout 2022.

Inflation will drop below 4% in the fourth quarter of 2022 and will reach the 3% central bank target in the first half of 2023.

Inflation is projected to be 4.7-5.1% next year and 2.5-3.5% in 2023.

Risks to inflation continue to be on the upside.

GDP

The recovery of the Hungarian economy will remain brisk, but growth in the coming quarters will be characterized by a dichotomy.

According to MNB's latest forecasts, GDP growth may be 6.3-6.5% in 2021, 4.0-5.0% in 2022 and 3.5-4.5% in 2023.

The central bank thus worsened its economic forecasts in September, due to the latest wave of the coronavirus and supply shocks.

The current account balance will improve rapidly as external markets and supply chains recover. New export capacities created in recent years will also contribute to this, Barnabás Virág explained.

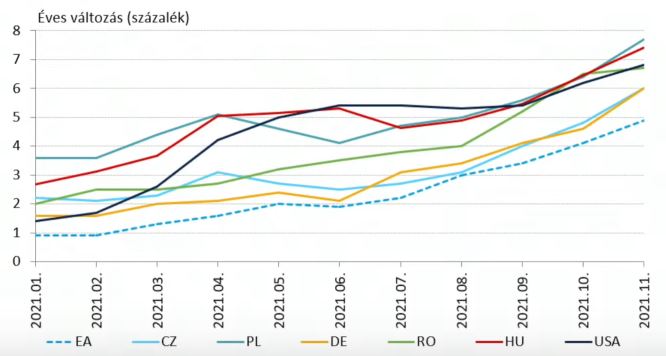

International inflation outlook

External inflationary pressures remain high and are expected to persist for several quarters according to MNB. In both neighbouring countries and developed economies, the rate of inflation is typically between 6 and 8 percent.

Inflation trends in international comparison