Above the clouds: What were the sources of growth reserves of the Hungarian economy?

EnglishAndrás BalatoniGéza RippelThough in December 2017 most analysts expected a slight deceleration in Hungarian economic growth, GDP increased by almost 5 percent in 2018, strongly outperforming the forecasts. This happened in a time when economic activity in Europe has been gradually losing its momentum. Exploring the sources of last year’s growth is important for several reasons. The analysis can help us to better understand Hungary’s economic growth, make forecasts more accurate and it contributes to the identification of growth factors in the coming years. This article is the first in a series by the experts of Magyar Nemzeti Bank, which aims to understand the economic convergence since 2013. Our first analysis focuses on the factors that determined the surprising GDP growth in 2018.

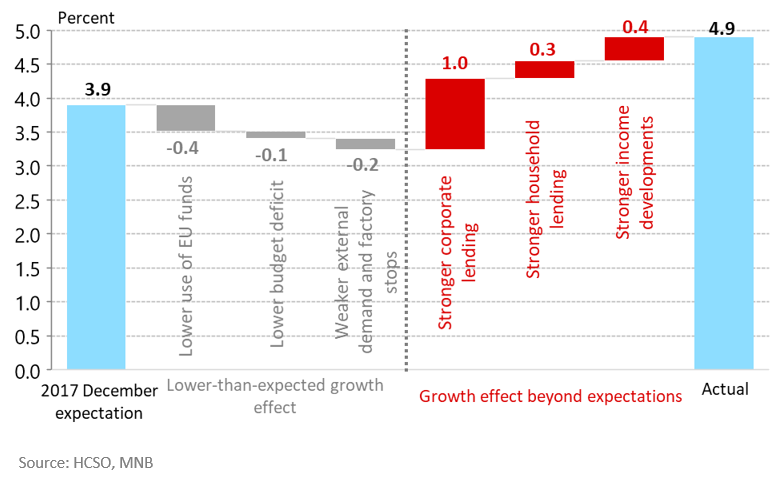

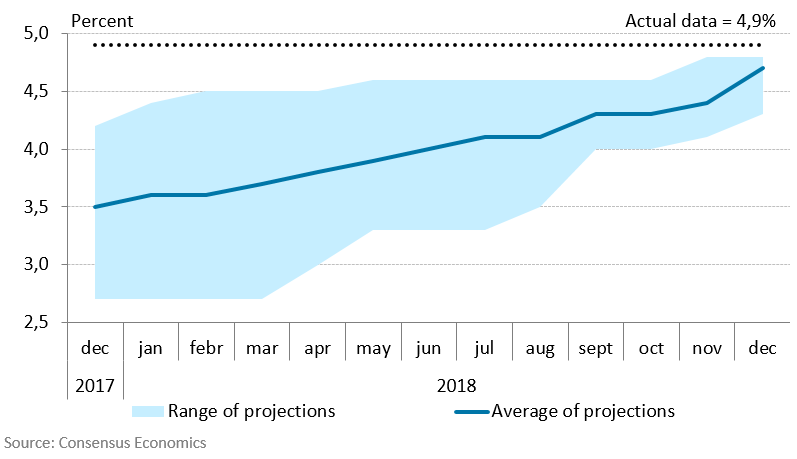

The Hungarian economy grew by 4.1 percent in 2017. GDP forecasts back in December 2017 expected growth rate between 2.7 and 4.2 percent for 2018, and the median was around 3.5 percent (December 2017 Inflation Report of Magyar Nemzeti Bank expected a growth rate of 3.9 percent). Overall, most of the analysts expected a slowdown in GDP growth. The preliminary flash estimate of the Hungarian Central Statistical Office was, however, that the Hungarian GDP grew by 4.9 percent in 2018. This means that Hungary is among the fastest growing European countries. This acceleration of economic performance was a major surprise to both Hungarian and international analysts. Although the forecasts continuously moved upwards last year, no analyst expected growth to be as rapid as observed (Chart 1).

Chart 1: Evolution of GDP growth forecasts for 2018

As a small open economy, economic growth of Hungary is determined by several factors. Changes in external demand, the utilisation of EU funds, the fiscal impulse, changes in household income and the expansion of lending play a major role in GDP growth. It is not a coincidence that almost all forecasts are based on these variables and the assumptions concerning them. Therefore, we analyse the surprisingly rapid growth of the last year by tracing back these presumptions.

We tried to trace back these assumptions and their impact on growth by relying on the most relevant sources in the respective fields. Data regarding external economic activity originates from Consensus Economics database; we relied on the Budget Act to assess EU funds and the fiscal impulse; finally, we assessed credit market and household loans relying on previous Inflation Reports of Magyar Nemzeti Bank.

The strong expansion of Hungarian GDP was shaped by several events that sometimes had opposing effects:

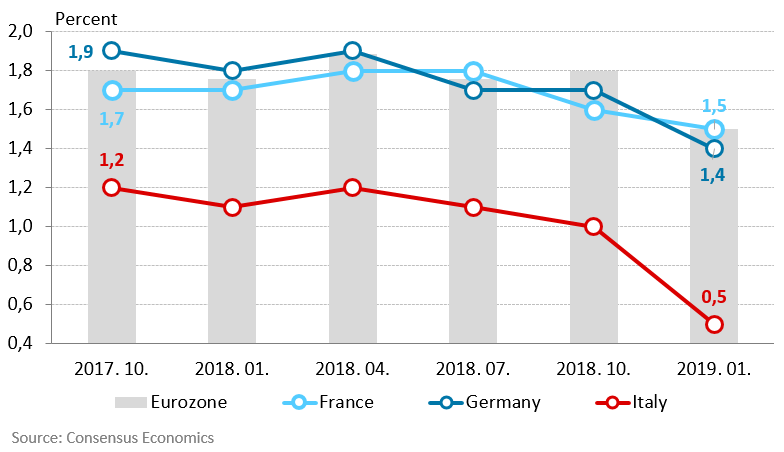

- The gradually escalating trade war, the poor performance of the German automotive industry and the uncertainties associated with the Italian economy and Brexit caused European economic activity as well as our major export markets’ demand to gradually lose momentum. Forecasts and estimations regarding the performance of major European economies gradually decreased during 2018 (Chart 2). Growth of our largest export partner, Germany, dropped by nearly 0.5 percentage points compared to end-2017 expectations. In addition to the poorer-than-expected economic output of our external markets, exports of the Hungarian automotive sector were held back by individual factory stops as well. Growth rate was 0.2 percentage points lower than expected due to weaker-than-expected external demand and Hungarian factory stops.

Chart 2: Evolution of GDP forecasts for major European economies

- We quantified the impact of EU funds on the economy based on the economic use of funds and not the total amount of funds paid to tender winners. It has broadly been assumed, that EU funds absorption will be high in 2018. Our estimation is, however, that nearly two-thirds of the payments could have been advance payments; therefore the related economic activity may occur later.

- Finally, the impact of fiscal policy on economic growth was also somewhat below the path specified in the Budget Act. The end-2017 budget forecast expected a 2.4 percent government deficit as a percentage of GDP in 2018. Revenues were higher than expected, and spending increased only at a lower rate. As a result, the government deficit as a percentage of GDP was lower than the target specified in the Budget Act. We estimate that the lower-than-expected utilisation of EU funds and the fiscal impulse would have caused a 0.5 percentage point lower growth rate in total.

The lower-than-expected effects on growth were, however, overcompensated by the effects of the credit market and the increase in household income.

- Since 2013, the corporate credit market, especially that of SMEs, has avoided a credit crunch, and it has entered an upward path in recent years. In 2018, lending expanded at a higher rate than expected in the whole corporate segment and also among SMEs (Chart 3). In 2018, SME loans were almost 12 percent higher than in 2017. In parallel with high capacity utilisation and low interest rate, buoyant corporate credit growth supported the dynamic rise in companies’ investment activity. Stronger corporate lending is estimated to have resulted in GDP growing almost 1 percentage point higher in 2018, which was indicated by the dynamically expanding construction output and machinery investment.

Chart 3: Annual changes in lending to non-financial corporations and SMEs

- In addition to the corporate segment, household lending growth also continued stronger than expected. The expansion affected both housing and consumer loans. The stronger-than-expected credit growth contributed to the buoyant expansion of household consumption last year.

- Higher household disposable income boosted not only consumption but also investments and financial savings of households. Household disposable income could have been considerably, almost HUF 1 000 billion higher than expected. More than 30 percent of that was attributable to higher labour income due to the dynamic wage increase, while higher pension premium in line with higher GDP growth accounted for another 10 percent. Almost 60 percent of disposable income was related to other incomes explained by higher incomes of entrepreneurs related to higher economic output. Previous experience shows that the increase in other incomes rather went to financial savings. GDP is estimated to have been higher by 0.7 percentage points due to stronger household lending and favourable income developments, which is also confirmed by the rapidly expanding household consumption.

Our overall conclusion is that the unexpectedly strong economic growth in 2018 was determined mainly by the credit market – mostly corporate lending – being responsible for nearly two-thirds of positive effects, and the more dynamic increase in household incomes increased it further. In the meantime, deteriorating external economic growth, lower-than-expected utilisation of EU funds and the lower fiscal impulse held growth back (Chart 4). The upcoming articles in our series will investigate the main factors underlying economic growth by explaining the impact of EU funds, the government budget, corporate and household lending and household income on economic growth in detail.

Chart 4: Factors explaining the higher GDP growth in 2018