The economic impact of the Magyar Nemzeti Bank programmes launched after 2013 is estimated to exceed HUF 10,000 billion

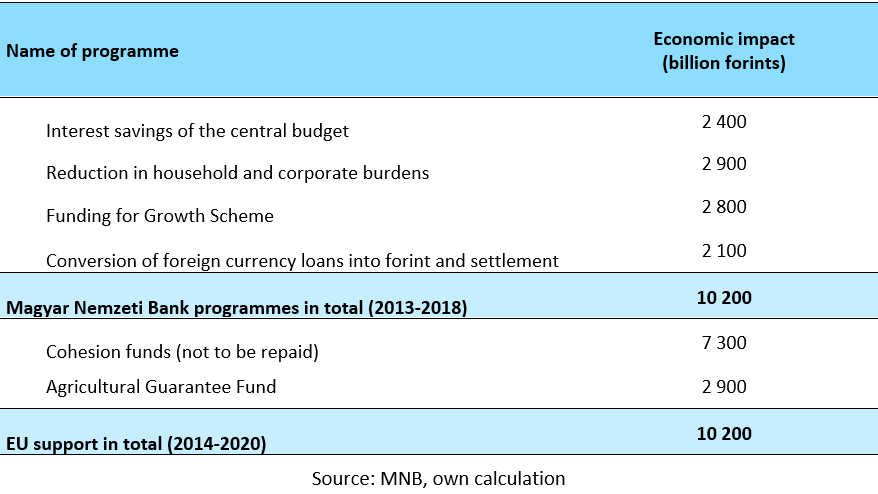

EnglishThe Magyar Nemzeti Bank programmes launched after 2013 resulted in saving and generating additional funds in the amount of HUF 10,000 billion for domestic economic agents until the end of 2018, which is basically identical with the amount of funds received from the European Union in the current 2014-2020 period. In addition to the savings and the availability of additional funds, the interest rate cut cycle of the Bank, the Funding for Growth Scheme, the Self-Financing Programme, the conversion of foreign currency loans into forint and further new instruments have several direct and indirect economic impacts, which will also be felt in the forthcoming years. In addition, the Magyar Nemzeti Bank was able to achieve all that while maintaining a continuously profitable operation.

The significance of the funds received from the European Union - which amount to approximately HUF 10,000 billion in the present budgetary period - for the Hungarian economy is common subject in economic analyses.

It must be added, though, that most of the articles about this subject are not thorough enough to show how much of these funds flow back to Western Europe, or at least to consider that Hungary pays HUF 300 billion every year to the common budget. It is even more important that they ignore the fact that over the past years, Hungary has mobilized funds of similar amounts from its own savings, or transferred funds, for instance, from loan repayments.

This article shows that the Magyar Nemzeti Bank’s programmes completed since 2013 had an impact on the economy of HUF 10,000 billion in total, i.e. basically the same as the EU funds.

The majority of these funds are interest savings achieved as a result of the easing cycle, and this appeared on the side of both the public finances and the private sector. Another saving is that the conversion of household foreign currency loans into forint prevented the threatening increase in instalments triggered by the stronger Swiss franc.

Finally, the first three stages of the Funding for Growth Scheme added loans of HUF 2800 billion to the economy, and this amount was used by small and medium-size enterprises for development and increasing the number of their employees. These savings and additional funds became available as a result of the targeted and innovative monetary policy of the Magyar Nemzeti Bank, renewed in 2013. In the following paragraphs, we are going to describe the key elements of these programmes.

1. Interest savings of the central budget

From 2013 to 2018, the central budget saved a total of HUF 2400 billion in interests.

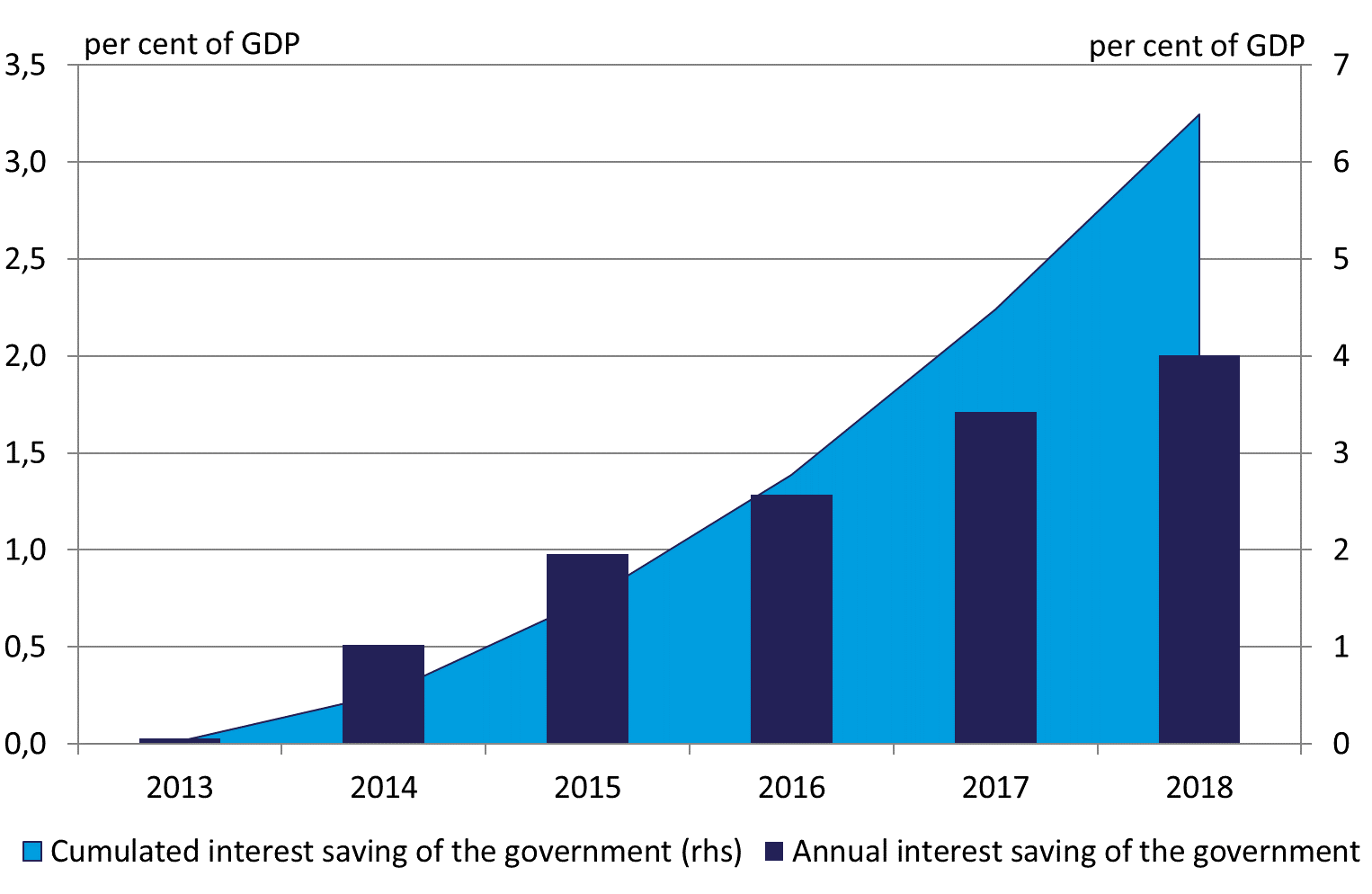

Due to the Magyar Nemzeti Bank's easing cycle, the Self-Financing Programme, the reform of monetary policy instruments, the lower inflation and the reduced risk spread, yields have declined significantly since 2013 in the government securities market. As a result of the Bank’s programmes and favourable domestic macroeconomic data, short yields dropped by 660 base points in average, while long yields dropped by almost 460 base points (as of August 2019).

As a consequence of significantly lower yields, the state's interest expenses dropped from 4.3 per cent in 2013 to 2.3 per cent in 2018, which generated a saving of HUF 800 billion in 2018. The accumulated savings realised since 2013 have amounted to 6.5% of the GDP, which means a total savings of HUF 2400 billion. In the low yield environment, the interest savings continuously increased, as public debts were gradually re-priced with lower yields. In 2019, the annual savings may increase to HUF 900 billion, which will further increase the accumulated savings.

Chart 1: Annual and accumulated state interest savings 2013-2018

Source: Eurostat, MNB

2. Reduction of households’ and companies’ interest burden

Households' and companies' burdens related to loans were reduced by approximately HUF 2900 billion in the period under review.

The reduction in interest burdens is nicely illustrated at macroeconomical level by the fact that on loans extended to households and companies, credit institutions realised interest incomes of HUF 304 billion in total in the second half of 2012, i.e. before the start of the easing cycle. In Q2 of 2015, i.e. after the settlement, this value shrank to HUF 184 billion. Between Q2 of 2015 and Q2 of 2018, further reduction was realised with the due to interest rate cuts, therefore the quarterly interest income realised on loans extended to the private sector was less than half of the value in the initial period, i.e. HUF 133 billion at the end of the period. The accumulated value of interest savings was HUF 2900 billion until the end of 2018.

It is important to maintain the achieved results, i.e. to make sure that the currently low interest burdens provide predictable instalments for both private and corporate debtors.

The Magyar Nemzeti Bank uses multiple instruments to support the spread of loans with interest rates fixed for a long term (Certified Consumer-Friendly Housing Loan, mortgage adequacy ratio, mortgage bond purchase programme, debt cap rules etc.), and this is also facilitated by stricter provisions on the payment-to-income ratio[1] and the MFL products[2] (Certified Consumer-Friendly Housing Loan) as of 1 October.

3. Funding for Growth Scheme

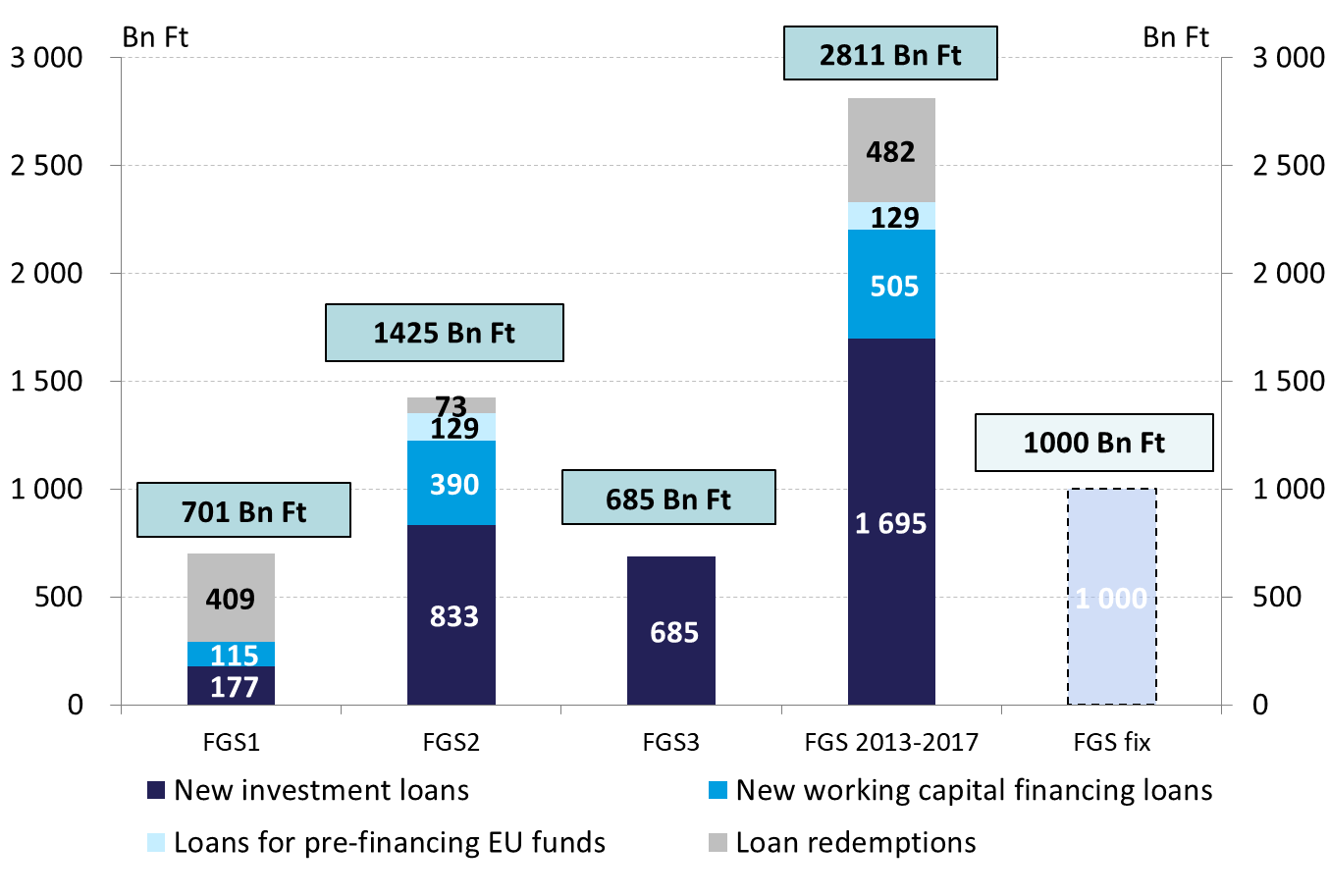

To restore SME lending, the Bank launched the Funding for Growth Scheme (FGS) in June 2013. In its three phases almost 40,000 SME's received favourable funding in the amount of over HUF 2800 billion.

As an important channel of the monetary policy transmission, the well-operating SME loan market is a basic condition of securing sustainable economic growth and financial stability. The programme played an important role in the fact that SME lending - which was characterised by a decrease after the crisis - started to gradually grow in the beginning of 2015, and then reached the growth rate of 5-10 per cent that is considered necessary over the long term by the Magyar Nemzeti Bank.

In addition to achieving a turnaround in lending, the FGS facilitated the spread of loans available for long term, with fixed and favourable interest rates, and free of exchange rate risk.

In the course of the three phases of the FGS, the emphasis was shifted to loans of investment purposes, and this facilitated the implementation of developments that made SME's more competitive. In the volume of SME lending, the phasing-out of the third phase of the FGS did not result in a setback, but the ratio of long-term loans with fixed interest rates dropped. Therefore, in 2018, the Monetary Council made a decision to launch the Funding for Growth Scheme Fix (FGS fix) product with a limit of HUF 1000 billion. With the new scheme launched in early 2019, the central bank seeks to influence primarily the structure of lending. The utilisation of the FGS fix reached HUF 100 billion in the beginning of May.

Chart 2: Amounts contracted in the individual phases of the FGS, and their division by loan purpose

Source: MNB

4. The conversion of foreign currency household loans into forint

The savings in the whole household sector may reach HUF 2100 billion during the whole term, as a result of the forint conversion and the settlement.

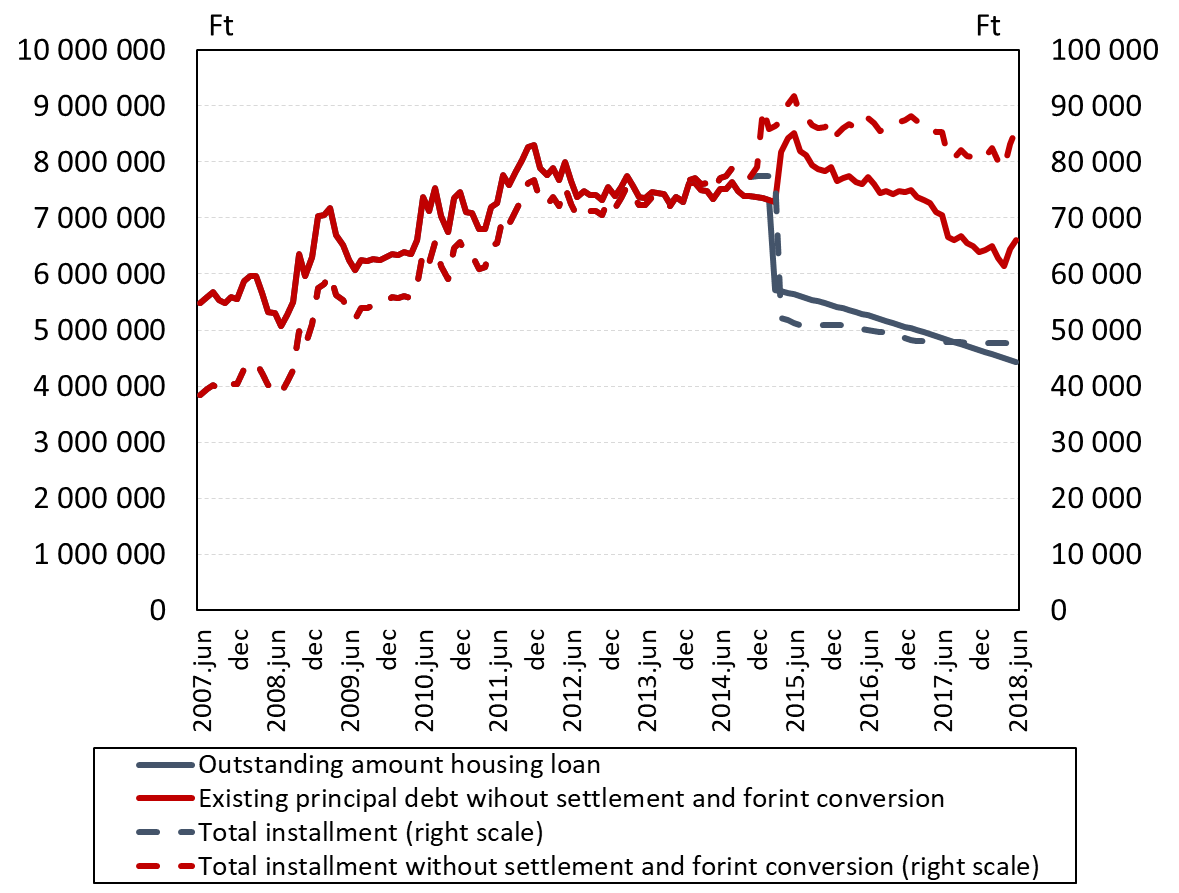

The significant savings can be calculated in a way that we aggregate the savings on foreign currency loan actions at macroeconomic level, and consider the fact that the exchange rate of the Swiss franc against HUF would be even higher than its present level because of the higher domestic vulnerability. If we examine the real repayment course of a typical debtor, and compare it with a scenario in which neither the settlement, nor the forint conversion would have taken place, we can see that the instalment of HUF 48 thousand to be paid presently would be almost 70% higher, i.e. over HUF 80 thousand.[1].

In the settlement with foreign currency loans, the Magyar Nemzeti Bank was an indispensable player in the process, as it worked out the detailed rules, continuously checked the model developments in the banks, and carried out the subsequent control of the settled amounts. In the process of forint conversion, the role played by the Magyar Nemzeti Bank was even more important, as the central bank made sure that the conversion would not cause any stress on the financial markets. This was achieved on the one hand with the tight coordination of the process, and on the other hand by satisfying the conversion-generated foreign currency requirements of banks from the foreign currency reserves.

Without these measures, several hundred thousand debtors would have had to endure the dramatic strengthening of the Swiss franc in 2015, which was caused by the Swiss central bank, as it eliminated the exchange rate threshold against the euro.

From 14 to 15 January 2015, the HUF weakened by 20 per cent against the Swiss franc, and since then it has not come even close to the exchange rate of the time of forint conversion. However, the HUF rate could have weakened even more, if the forint conversion had not been technically completed already in the previous quarter: at that time, the vulnerability of the country would have been much bigger because of the significant open positions of households, which would have resulted in a more intensive weakening of the exchange rate. In addition, in the lack of any settlement, consumers should have been obliged to pay the impacts of the unilateral interest rate increase, which would have meant 25-30 per cent higher instalments.

Chart 3: The development of the instalment and the existing principal debt in the case of a typical, always performing mortgage loan, with foreign currency loan measures and without them

Source: MNB

5. Summary

Due to the interest reduction cycle of the central bank, the Funding for Growth Scheme, the Self-Financing programme, the conversion of foreign currency loans into forint and further newly introduced instruments, savings and additional funds of HUF 10,000 billion were generated in the domestic economy until the end of 2018. This amount is basically identical with the amount of funds received from the European Union in the present EU budgetary cycle. It is important to note that the economic impact of 10 thousand billion forints came in parallel with the continuous profitable operation of the central bank, and this amount may further increase in the following years.

Table 1: The economic impact of central bank programmes and EU supports

Figures in HUF billion

[1] A payment-to-income repayment indicator differentiated by interest period was introduced. https://www.mnb.hu/sajtoszoba/sajtokozlemenyek/2018-evi-sajtokozlemenyek/az-mnb-az-adossagfek-szabalyok-modositasaval-is-osztonzi-a-fix-kamatozasu-lakashitelek-ternyereset

[2] As of 1 October 2018 loans with 3-year interest rate periods were taken out from the scope of MFL products, and at the same time, credit institutions were allowed to start the distribution of MFL products with interest rates fixed for 15 years.

[3] The details were earlier described in the article titled https://www.mnb.hu/letoltes/15-06-05-fabian-gergely-mit-usztak-meg-pontosan-a-deviza-jelzaloghitelesek.pdf.