The Hungarian government might tighten the most popular tax scheme among sole proprietors as of 2021

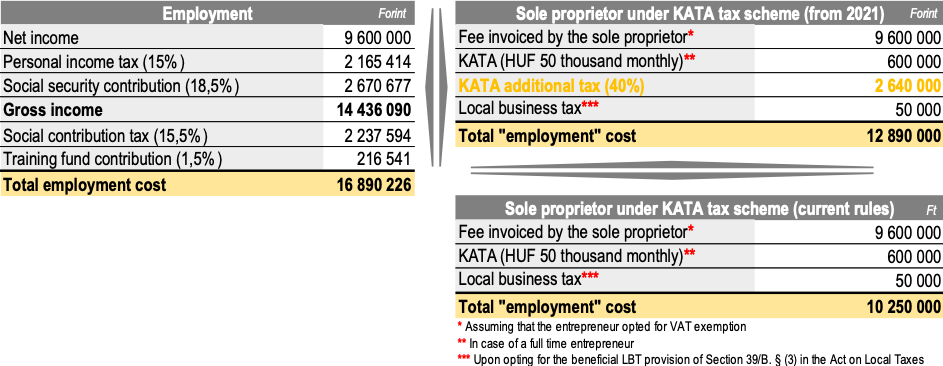

EnglishThe rules of KATA will become stricter from the next year: if an entrepreneur opting for KATA issues invoice(s) to the same party in a value exceeding 3 million forints on an annual basis, an additional tax of 40% will be applicable. The stricter rules might decrease hidden employment, however, in overall, it might be still beneficial to opt for KATA from a tax perspective. We will illustrate the expected effect of the changes through a high-level numeric example.

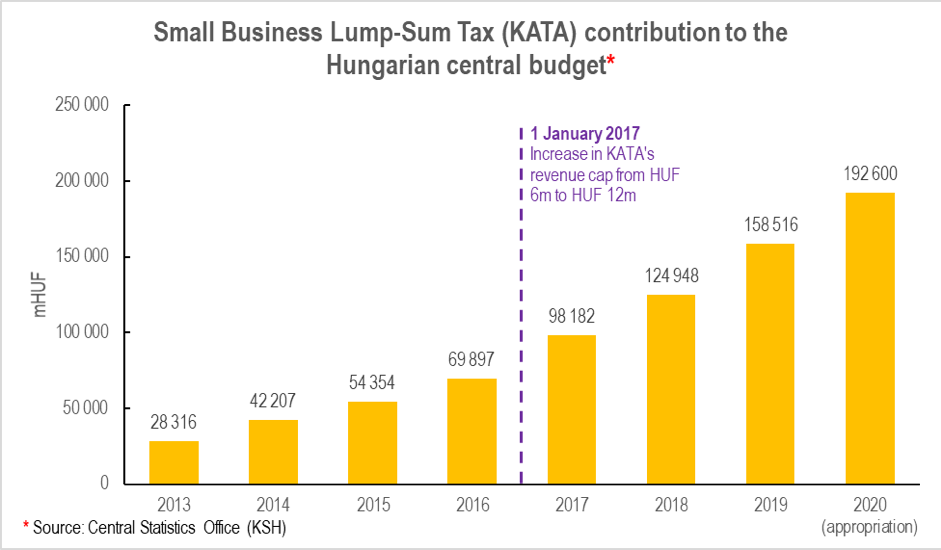

The small business lump-sum tax (“KATA”) has quickly become the favorite tax scheme among sole proprietors since its introduction in 2013 due to its simplicity and relatively low fixed amount. Full time entrepreneurs opting for KATA may replace their corporate income tax, personal income tax, vocational contribution and social contribution tax liabilities by paying 50 thousand forints on a monthly basis (opting for VAT exemption is also possible).

As outlined in the official explanation of the respective act, the original goal of the KATA was to simplify the taxation of small businesses and decrease the tax avoidance.

However, the inflation of the fixed lump-sum tax of 50 thousand forints and the increase in KATA’s revenue cap from 6 million to 12 million forints made the hidden employment through KATA more attractive to medium and large enterprises.

This is also supported by the analysis prepared by the Ministry of Finance, according to which in 2013 only 3% of the KATA taxpayers were employees before, although, this rate increased substantially by the end of 2019: approximately 40% of the 377 thousand entrepreneurs – registered as KATA taxpayers – were employees just before becoming entrepreneurs.

The extra budgetary expenses triggered by the coronavirus pandemic and lower expected budgetary revenue put the tax abuse into spotlight: the hidden employment via KATA needed to be curbed.

During a press conference on 25th of June, Gergely Gulyás unveiled the government’s plan of modifying the rules of KATA from January 2021: “If somebody opts for the KATA tax scheme and issues invoices to the same party in an amount exceeding 3 million forints, 40% tax should be paid for the exceeding part”. The Minister of the Prime Minister’s Office told that their aim is to abolish the abuse with KATA and the hidden employment.

For example, if a KATA taxpayer invoices 800 thousand forints to his/her former employer on a monthly basis (9.6 million forints annually), 2.64 million forints of additional tax should be paid on top of the monthly fixed lump-sum tax of 50 thousand from January 2021.

Even though the potential “saving” might be lower compared to regular employment under the modified rules, opting for KATA can be still beneficial even by paying 40% additional tax on the revenue exceeding 3 million forints.

This is because the additional tax of 40% is still lower than the total tax burden of 76% applicable on the net income in case of a regular employment (taxes & contributions payable by the employer and employee altogether).

Although, there are still some open questions in relation to the upcoming changes. For example, the press conference of the government did not reveal whether the invoices issued to related parties should be consolidated when calculating the tax base of the 40% additional tax. If no, the additional tax may be avoided by deriving revenue from multiple related parties in an amount less than 3 million forints respectively. Having regard on the fact that invoices issued to related parties should be consolidated even under the current rules when reporting the invoices with an amount exceeding 1 million forints, the legislator will likely give special attention to the prevention of tax abuse via related parties during the upcoming changes.

Lastly, there is still room for fine-tuning the detailed rules of the KATA-tightening after reviewing the feedbacks and comments received subsequent to the press conference. We have seen similar during the state of emergency, when the government considered the observations raised by the economic operators regarding the Hungarian wage subsidy scheme (“Kurzarbeit”) and amended the concerned government decree accordingly.