Bertelsmann Foundation, Unimpressed by Actual Facts

EnglishWhile factual and comprehensive assessments of the macroeconomic fundamentals are growing more and more important in today’s turbulent global market environment, some organisations that like to consider themselves as authorities on the subject tend to disregard objective statistics. This paper has been inspired by the latest country report released by the Bertelsmann Foundation, which can be considered as a subjective opinion of practically just two (yes, 2) analysts. Although the fundamentals of the Hungarian economy have been improving exceptionally dynamically thanks to the reforms of the past decade, creating the foundations for a sustainable convergence, the Bertelsmann Foundation is more appreciative of the economic policy that drove Hungary into a debt crisis in the 2000s. The self-contradictions and shortcomings of the report stem from the use of a methodology including a variety of dubious elements.

The Bertelsmann Foundation’s 2020 country report is a common example of how black can be presented as white and vice versa.

This is because according to the Bertelsmann Foundation’s Transformation Index (BTI) Hungary’s performance deteriorated since 2006 in 44 of the 49 aspects reviewed – including the stability of the fiscal, the monetary and the financial system – and it has not improved in the remaining 5 areas either. The Foundation’s statements are shocking for all those who know and keep up with developments in Hungary’s labour market, fiscal position, income, lending and other economic areas. The following is an attempt at presenting a more accurate picture of the past fifteen years of the Hungarian economy based on some key indicators noted in the country report but not taken into account with the appropriate weight, refuting many of the statements presented in the analysis.

Criticism of the methodology

Before outlining the conclusions it is worth taking a close look at the methodology underlying the Bertelsmann Foundation’s analysis because it explains many of the distortions in their results. No factual data appear directly in the BTI’s quantified evaluation; instead, each indicator reflects a subjective value judgement, each based on the opinions of only two (that is, 2!) analysts. (The precise technical description of the process is to be found on the methodology sub-page of the BTI website, at this link)

Although the textual part of the country report contains a description based on real data, and at some points it even recognises the achievements of the Hungarian economy, but the numerical evaluation and ranking is not in line with this.

This is an unprecedented approach even in comparison with the methodologies underlying international competitiveness rankings relying heavily on results of subjective assessments as well besides objective indicators. While the justification of taking certain subjective assessments into account can be questioned even in the case of such rankings, at least the methodologies applied in those cases appear to be more coherent on the whole. The BTI’s quantitative evaluation, however, is based on the opinions of only two experts instead of factual data, so the BTI can (and do) have any value they like. This approach is problematic in several aspects. On the one hand, two experts can hardly have a proper in-depth insight into the broad areas covered by the country report (including political institutions, monetary policy, education, research and development, environmental protection, international relations etc.) and on the other hand, on such a limited sample individual opinions have a massive distorting effect on the results. Subjective elements that are unavoidable on an individual level could be eliminated by having the methodology based on interviewing or surveying a wide range of respondents; and where objective indicators are available, those should be taken into account. Without that, there are multiple contradictions between the text and the quantified results of the country report and the report makes a selective choice between facts and opinions. Consequently, Hungary’s scores indicate a deterioration in the country report in a number of specific areas where progress has indisputably been made. The following is a discussion of processes that have actually been taking place and these most salient contradictions in the economic aspects of the report.

How the Bertelsmann Foundation illustrates the years of decline before 2010

The period between 2002 and 2010 was characterised by high fiscal deficit, low employment rate and financial vulnerability. Indeed, while mismanaging domestic risks the responses to the global financial and economic crisis of 2008 given by the economic policy were all inappropriate.

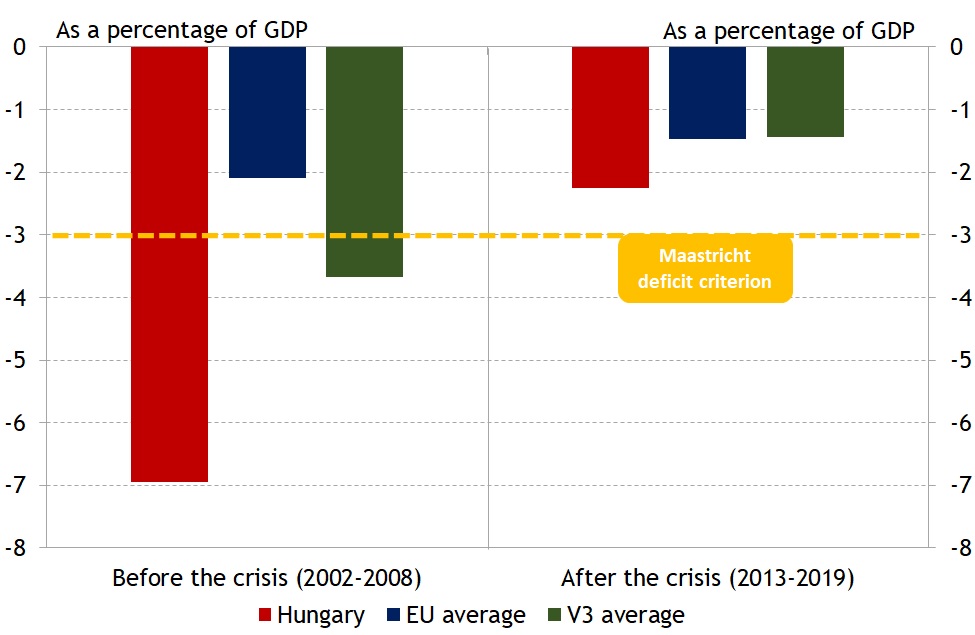

The unreasonably procyclical fiscal policy pursued during the period under review resulted in a fiscal deficit of an average of about 7 percent of GDP between 2002 and 2008, in an exceptionally favourable global economic environment (Chart 1). The unhealthy economic structure was reflected by the fact that despite such a degree of fiscal stimulus, Hungary's average growth rate (of 3.3 percent) lagged behind the average of other countries in Central and Eastern Europe (5.3 percent) and that Hungary registered one of the lowest employment rates in the EU (Charts 2 and 3). As a result, from its leading position in the region in the early 2000s, Hungary had fallen behind its competitors by the end of the decade and faced with the global crisis in 2008 with a steeply rising public debt and a foreign currency debt threatening the national economy as a whole. Between 2002 and 2010, decision makers at that time sacrificed macro financial balance first in order to encourage economic growth and then tried to manage crises as internal and external risks were materialising by introducing restrictions: eventually, their attempts at achieving economic balance and sustainable growth equally failed. It is more than surprising, therefore, that Bertelsmann’s experts rate the economic performance at that time 8 on a scale of 10, the same as recent years’ really successful economic performance which we will discuss in more detail later on.

Chart 1: Annual average budget balance-to-GDP ratio before and after the 2009-2012 global crisis in Hungary, in the V3 region and the European Union

Source: Eurostat

The years after 2010, or how Hungary recovered its leading position

The change in the economic model in 2010 and many structural reforms resulted in fiscal and economic stabilisation through an extensive activation of the labour market.

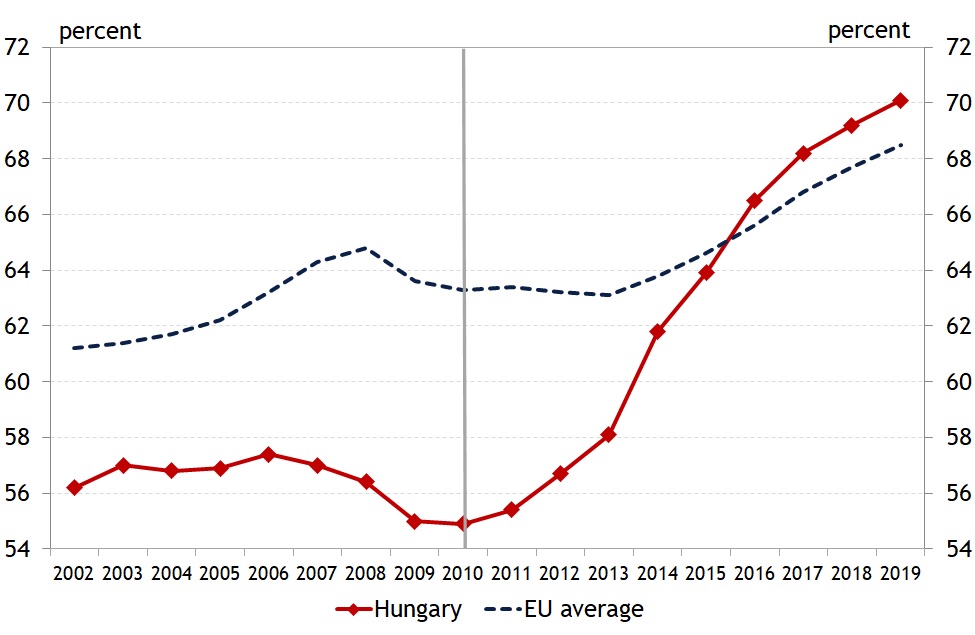

The new economic policy has recognized that without stable growth, sustainable fiscal balance cannot be achieved; it therefore introduced fiscal reforms simultaneously stimulating the economy and keeping the government budget under control. The efforts aimed at achieving the two targets simultaneously relied on the necessary increase in employment. Structural reforms shifted the focus of taxation system from taxes on labour towards consumption type taxes which are less of an impediment to employment and competitiveness. In addition to the introduction of a flat personal income tax system and the family tax allowance system, the supply side of the labour market was stimulated also by social benefits, rationalised in the context of the budget’s supply side reform (through the so-called “Széll Kálmán Plans”). Demand for jobs was boosted through the Job Protection Action Plan, providing up to 900 thousand people with jobs in some years and public employment programmes. The reforms led to a successful turnaround in employment. The rate of employment in Hungary – the lowest in the EU in 2010 – exceeded the EU average by 2019 (Chart 2).

Chart 2: Employment rate in the 15-64 age group in Hungary and the European Union

Source: Eurostat

The fiscal reforms stimulating employment and growth, introduced from after 2010, brought the fiscal deficit to a persistently low level of about 2 percent from 2012, a very significant improvement over the situation in 2006 (Chart 1).

Indicating the effectiveness of the comprehensive reforms in the structure of taxes and expenditures, the primary fiscal balance was positive for the first time again after 12 years. In 2013, Hungary was even released from the then 9-year excessive deficit procedure. Hungary’s budget deficit-to-GDP ratio was 9.3 percent in 2006, while in 2019 the corresponding ratio was down at 2 percent. The BTI country report’s fiscal section contains some particularly pronounced contradictions. While even the analysis admits that the fiscal deficit was high around 2006, and that by contrast the recent years have been a period of fiscal discipline and faster economic growth, we find it simply impossible to understand how they can nonetheless assess a score of 8 to fiscal policy in 2006 and a score of 7 to that of 2020.

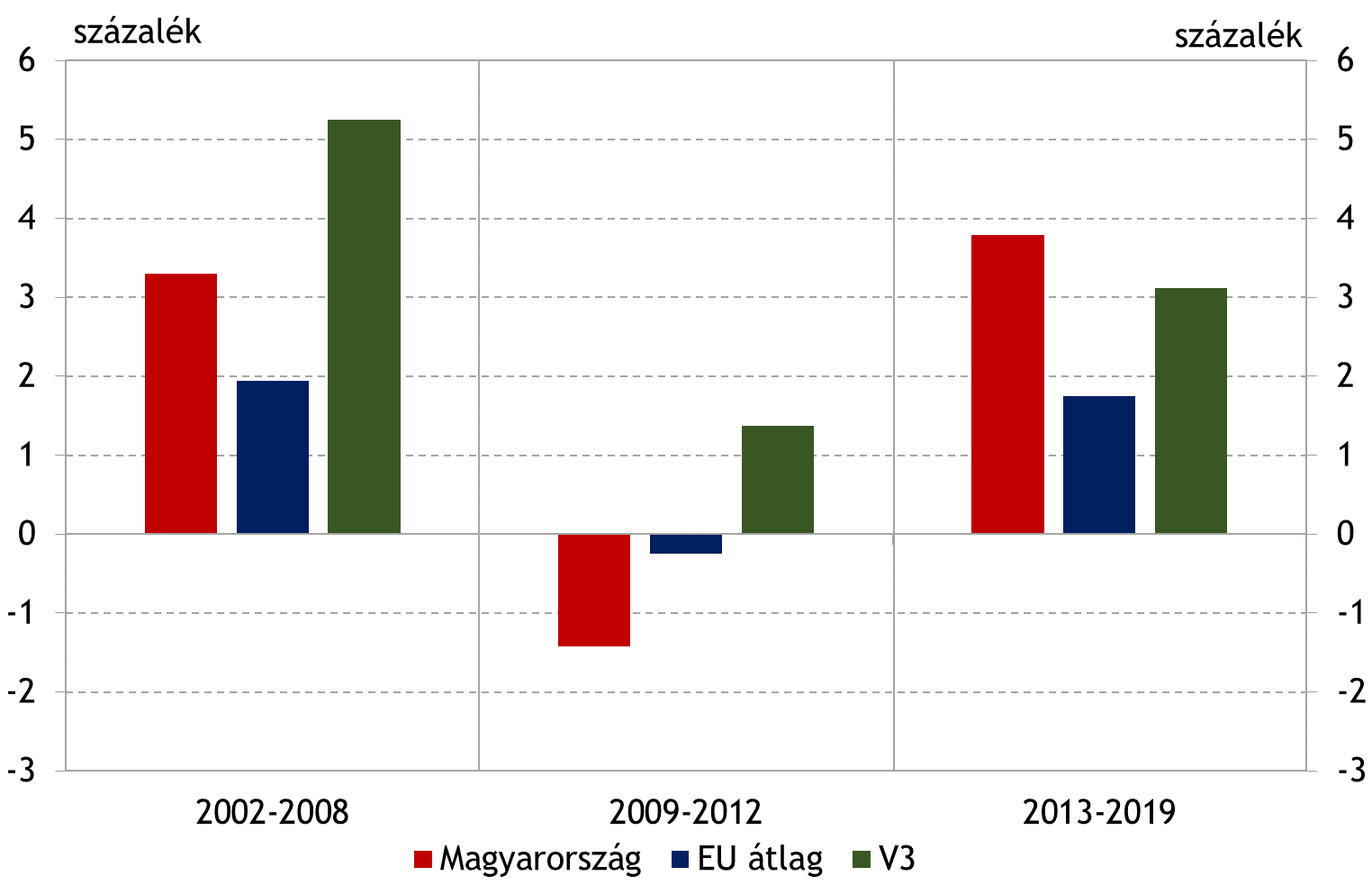

By successfully applying the formula of economic balance and growth, Hungary has set out on a sustainable convergence path since 2013, growing even more dynamically than our competitors.

Since the turnaround in growth in 2013, the Hungarian economy has grown at 3.8 percent a year on an average, more than 2 percentage points faster each year than the EU average (Chart 3). Sustainable dynamic economic growth and continued improvements in competitiveness are driven by an increase in the investment rate: in 2019 Hungary’s rate was the second highest (28.6 percent) in the European Union. The 8.5 percentage point increase in this ratio since 2010 was also the second highest in the EU. Inconsistently, while the country report describes how economic growth reached its highest rates during the past few years since the political and economic transition of ‘89-‘90 and how unemployment has reached record lows and employment increased, the country’s economic performance today is still assigned a score of 8 just like that of 2006 (despite the fact that practically almost everything but this score has improved).

Chart 3: Annual average GDP growth rates before and after the 2009-2012 global crisis, in Hungary, in the V3 region and the European Union

Source: Eurostat

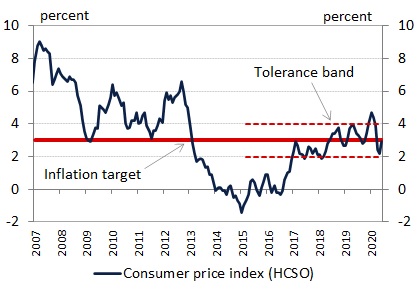

Catching up while maintaining macro-financial balance could not have been possible without the 2013 monetary policy turnaround: since then the central bank has contributed about half of economic growth.

By proactively applying conventional and some non-conventional tools, the MNB managed to stabilise inflation, that has been developing, for the most part, within the tolerance band around the 3 percent target since early 2017 (Chart 4). In addition to achieving this, Hungary's external vulnerability has also been reduced significantly, not least as a consequence of the MNB’s targeted programmes (e.g. Self-financing Programme). The coordination of fiscal policy with monetary policy is reflected by both the successful phasing-out of household foreign exchange loans and a substantial decrease of the government interest expenditures. As a result of the prevailing favourable monetary conditions, the interest expenditures of the government decreased steadily and considerably between 2013 and 2019 (the second most substantial decrease in the Union), saving government interest spending of a total of about HUF 3,500 billion. The text of the country report similarly contradicts the quantified evaluation regarding fiscal policy as it does when it comes to its evaluation of monetary policy. For, while admitting that the population’s indebtedness in foreign currencies during the 2000s increased vulnerability and that in recent years this could be eliminated by converting foreign exchange loans into HUF, and that the inflation rate is steadily around the target (which used to be otherwise for most of the time), yet they evaluate a score of 8 to current monetary policy, while they give 9 points for the monetary policy between 2006 and 2012. Moreover, some assertions are indicative of the authors’ inadequate knowledge of the applicable legal regulations. This is because they explain the lower score for monetary policy by arguing that the central bank supports the government’s economic policy! As a matter of fact, however, the MNB has no other option, being the bank of the Hungarian nation; Section 3 of the MNB Act provides that, in addition to attaining and maintaining price stability, the MNB is also required to use all available instruments to support the government’s economic policy.

Chart 4: Inflation in Hungary, over time

Source: HCSO

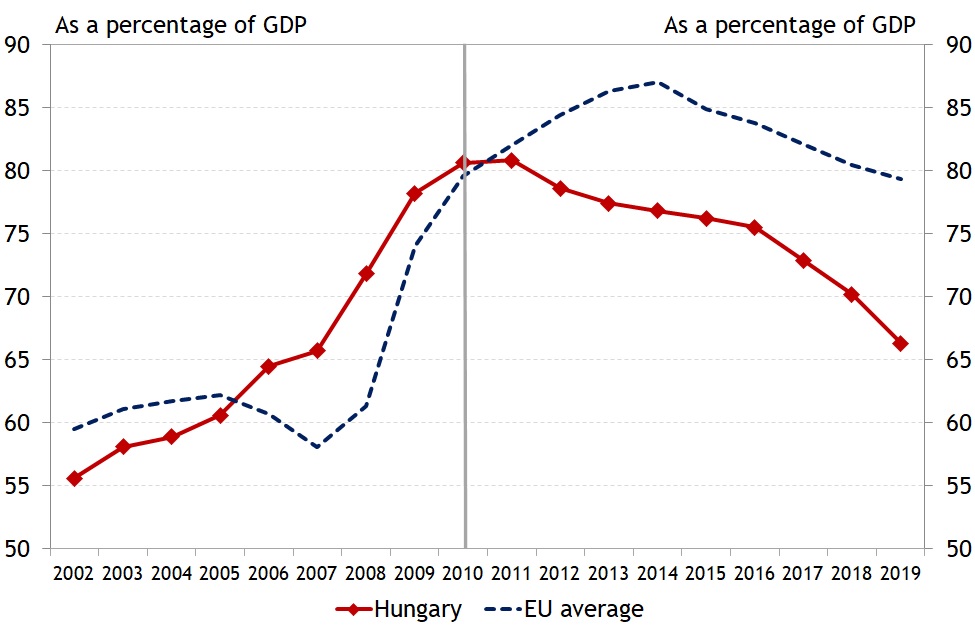

Both fiscal stability and the existing favourable and sustainable macroeconomic structure are reflected by the downward trend of Hungary’s public debt-to-GDP ratio.

In the wake of a disciplined fiscal policy and dynamic economic growth since 2013, the public debt-to-GDP ratio dropped from 80.8 percent in 2011 to 66.3 percent by end-2019, the fourth most substantial decrease in the Union. Hungary is the only Member State in the European Union whose public debt has decreased every single year since 2011. Moreover, the structure of public debt also improved considerably, reducing Hungary's financial vulnerability. Up to 2011 about two-thirds of central government debt was owed to foreign creditors, and about 50 percent of total debt was denominated in foreign exchange. Thanks to the debt management strategy adopted after 2011 with a focus on the conscious strengthening of the domestic investor base and the supportive programmes launched by MNB after 2013, the ratio of foreign ownership had dropped to a historical low of 34 percent at end-2019, and so did the foreign currency ratio, at 17 percent. Such a dramatic reduction in Hungary’s external financial vulnerability has become particularly valuable by today, when an unprecedented external shock has hit the entire global economy.

Chart 5: Gross public debt-to-GDP ratio in Hungary and the European Union

Source: Eurostat

Societal conditions improved remarkably in comparison to the situation before 2010, in parallel with the outstanding performance of the work-based and investment-friendly economy.

Building up a broadly work-based society was a central element of the post-2010 reforms to replace the preceding decades’ economic model based on subsidy and sustained by external financing. Through programmes stimulating employment and the economy, Hungary has come close to full employment. Wage growth resulting from broad-based employment and a tight labour market made a substantial contribution to reducing the ratio within the total population of those facing the risk of poverty or social exclusion. However, the Bertelsmann Foundation claims are also contradictory in this area. The country report heavily criticises the welfare system in relation to which it quotes Eurostat statistics regarding the share of the population of those facing the risk of poverty and social exclusion. Remarkably, the authors describe certain elements of the complex system of indicators without noting how the composite indicator has dropped in Hungary from 31 percent in 2006 to below 20 percent, below the EU average of 22 percent.

Moreover, the written analysis asserts that Hungary is one of the most unequal societies within the European Union while admitting the fact that income inequality in Hungary is below the EU average.

Remaining on the ground of facts, staying committed to sustainable convergence

Economic policy goals and the professional discussion accompanying the road towards them can often lead to constructive results; however, common recognition of the results as evidenced by objective indicators is an indispensable prerequisite.

Any starkly different approach will not only distort the analysis of past results and processes but can also have an unjustifiable negative impact on the current views of a given country, and it eliminates even that common denominator on the basis of which constructive professional debates could be conducted on the future path of development. And what facts show is that the accomplishments of the Hungarian economy during the past decade are, indeed, outstanding, not only in terms of domestic economic history but also by international standards. The fundamentals for sustainable development are now given in Hungary, to which the reforms proposed also by the central bank to further improve competitiveness may constitute another essential pillar.

The MNB continues to offer its services in terms of objective and professional analyses of the situation and in explaining the facts and considerations underlying the relevant economic policy actions.

The temporal and international comparative analyses and studies released by the Magyar Nemzeti Bank are always based on facts. In case anybody has any question concerning the achievements of the recent years, particularly in comparison to the unfavourable macroeconomic processes before 2010, we recommend comprehensive and in-depth analyses of objective statistics, for all analysts.

The authors are experts of the MNB.